How to know when housing bottom is in

New homes at the Cielo at Sand Creek by Century Communities housing development in Antioch, California, U.S., on Thursday, March 31, 2022.

David Paul Morris | Bloomberg | Getty Images

Chicago realtor Jeremy Fisher headed to Florida after Christmas counting on five mostly-relaxed weeks, after a slow second half of 2022 left him with a bunch of unsold listings exiting the year.

Instead, the Compass broker ended up flying back to the Windy City three times during his low season, as seven homes went into contract and his husband ended up driving their baby home from Florida alone. The great real estate bust, it seems, has found something like a floor.

“For somebody, it’s always the right time to buy a house,” Fisher said. “People for the most part have come to terms with interest rates.”

After only a few months in the tank, is the U.S. housing market close enough to a bottom that it’s time for those on the sidelines to at least start thinking about buying as spring shopping season nears?

Signs are accumulating that the big price bust — and mortgage-rate relief — that buyers wanted isn’t materializing, at least not soon.

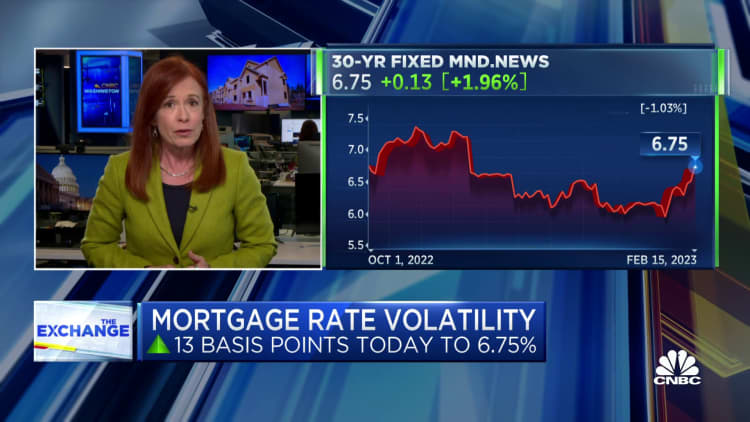

Goldman Sachs trimmed its estimate of peak-to-trough declines in nationwide home prices to 6 percent from 10 percent in late January. Online housing marketplace Zillow now expects prices to rise slightly in 2023. Existing home sales, which were running at a 6.5 million annual pace in early 2021, have begun to stabilize around 4 million, with the National Association of Realtors forecasting 4.8 million for the year. Meanwhile, mortgage rates, which dipped under a 6 percent national average on Feb. 2 after more than doubling since mid-2021 to almost 7.4 percent, have jumped back to 6.75 percent, driven by a scorching January jobs report.

No bust, but a standoff between buyers and sellers

Instead of a price bust a la the one after the mid-2000s housing bubble, what’s developing is a standoff, says Logan Mohtashami, lead analyst for HousingWire in Irvine, Calif. On the one hand are buyers who would like homes to be as affordable as in 2019. But a big share of them either have to move or can afford to despite higher prices and rates. On the other are sellers, under no pressure to move since they have cheap mortgages and plenty of equity for now. So far, sellers are hanging tough in most cities. Even small increases in demand can keep prices firm, or move them higher, because inventory is so tight, Mohtashami said.

The recipe for 2023’s housing market is shaping up as prices that are roughly stable nationally, but with ongoing drops in some regional markets, interest rates that decline but not hugely, and buyers’ incomes that rise. Experts think they will combine to make affordability improve, maybe to near-normal historical levels, but still fall well short of where home buyers stood when mortgage rates were 3 percent or even lower.

“Households have two incomes, and you have to earn about $100,000 to buy a house,” Mohtashami said. “There are lots of dual-income couples that can do that. It gives you more buying power than people know about.”

No return of 2008, or 3{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb} mortgage rate

The biggest reason why housing prices aren’t plunging like they did after 2008? Because the market isn’t being flooded with homes that drive down prices, as happened then.

Capital-rich banks aren’t under pressure as they were then, with foreclosure rates less than a tenth of those from the housing bust. Neither are households, with debt payment burdens near historic lows and few homeowners owing more on their mortgage than the house is worth. Serious delinquency rates, which skyrocketed after 2006 and led to 6 million foreclosures, have fallen by nearly half in the last year, to less than 0.7{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb} of mortgages, according to Fannie Mae. Unemployment is the lowest in 54 years, letting homeowners either trade up or hang on to their current homes easily – and if they are among the 85 percent of owners whose mortgages carry interest rates below 5 percent, many will stay put rather than buy a more expensive house with a costlier loan.

All that means the supply of homes for sale is likely to stay tight, which limits price declines.

Affordability is bad now, after rate hikes and Covid-driven price increases, but it has been worse. And we’ve all been spoiled by recent history: After the financial crisis, housing affordability nationally literally doubled as interest rates collapsed and prices fell, reaching all-time highs. It had retained most of those gains up until the Covid price surge, even as home values recovered.

“Rates will be dropping in the second quarter, but we don’t see a drastic drop that should make people wait,” said Nadia Evangelou, director of real estate research at the NAR. She predicted that 30-year mortgages will decline to around 5.75 percent. “Buyers realize 3 percent rates are not coming back.”

Housing affordability is stretched

The NAR’s closely-watched affordability index, which considers prices, rates and buyers’ incomes, is much lower than in 2019, but is still in line with the late 1980s and early 1990s. At current levels, the Housing Affordability Index says the median buyer can afford the median U.S. home — but barely. In 2020, the median buyer could afford the median home with a 70 percent cushion, which was the product of 3{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb} loans, Covid-driven income support and the residual impact of big home price drops between 2006 and 2011. Since 1980, the average is that median home buyers have about 20{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb} more income than they need for the median home, Evangelou said.

So why is anyone buying homes that are suddenly less affordable?

For Maggie Neuder, a client of Fisher’s in Chicago, the answer boiled down to wanting a new place and being able to afford one. Having seen 6 percent interest rates when she bought her first place in 2007, she’s not daunted by today’s rates, she said. The 41-year old finance executive bought a bigger home than she needed during Covid to ride out quarantines, and now wants a smaller place in the city’s Lincoln Park neighborhood, so she executed a flip.

To calm her buyer’s interest rate fears, she is giving a closing credit big enough to buy down the mortgage rate on the buyer’s loan for the first two years, by two percentage points in year one and one percentage point in year two – a move many builders are also using to sell new homes. To make back the money, she extracted a similar concession from the seller of the home she expects to buy in April.

“People look at refinancing like it’s a bad thing,” she said, figuring she can likely lower her payment within a couple of years. “I don’t think we’re going back to the sub-threes, but somewhere in the fours. Even if rates don’t fall below 6, I’m in a comfortable place with my mortgage.”

Fisher says his recent buyers fall into three camps. At either end are first-time buyers who have never had a 3 percent loan, and older buyers who are paying cash. Neither is much bothered by rates around 6 percent, he said. In the middle are move-up buyers who initially worried about rates more. But they are making work-arounds like Neuder’s to get what they want, Fisher said. These buyers likely drove the increase in applications for new mortgages that happened as rates fell earlier this winter.

“People have wrapped their heads around where interest rates are, and they have adapted,” Fisher said.

Indeed, combining the wage gains of the last few years with the deflation that has begun to show in market-based housing data in the last six months, and the most flagrant cases of distorted regional markets have begun to correct already. Another boost comes from solid rates of new household formation, said Daryl Fairweather, chief economist at Redfin.

Where home prices are now

The average house price is down 6 percent since the June peak, according to the S&P Case-Shiller index of prices in 20 major metro areas, and 3.5{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb} in the index for the whole country.

Recently-hot markets have taken bigger hits, as expected. In San Francisco, the Case-Shiller index is down 12 percent, in Phoenix 8 percent. In Sacramento, home prices have given back almost half of their Covid-era gains, said Ryan Lundquist, a local appraiser who blogs about the market in California’s capital. In metro Tampa, where prices rose 69 percent during Covid, according to Case-Shiller, prices are down only 3 percent.

Add in wage growth — wages rose about 5 percent last year, according to data from Zillow — and the effective price of housing has come down sharply in some places, while remaining well above pre-Covid levels, Zillow chief economist Skylar Olsen said.

“Even with values down a bit since August, if you bought the average house in February 2020 you have annual gains of 11 percent,” Olsen said.

Wage growth is one reason why even in some recently-hot markets, buyers are still out there, said St. Petersburg, Fla. broker Jeffrey Clarke. Indeed, he recently talked one client with a home in another city out of selling their place in St. Petersburg, convincing them that the crash they feared was not coming.

By the NAR’s numbers, affordability is now poor in metro Tampa, with the median buyer only earning 80 percent of what’s needed to buy the median home. But Tampa is close enough to equilibrium that Clarke doesn’t see anything coming like 2008-2011, when the average Tampa house lost half of its value.

“With nothing falling yet, no one is freaking out,” he said.

The math on mortgage rates and wage growth

The big flaw in the thesis that only minor price drops are coming is that so many large regional markets like Tampa remain out of line with local incomes, and many of them were in much better balance as recently as two years ago. Another is that San Francisco, Phoenix and Las Vegas all saw more than a 1{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb} price drop in January alone, according to Zillow, making forecasts for relatively-stable prices look shakier.

Much of Florida and Texas, and markets like Asheville N.C. and Denver, had relatively-affordable housing until 2020 but median homes are now 20 percent to 30 percent too expensive for median local incomes, according to NAR data released in October. In much of California, NAR affordability indexes are at 50 or below, indicating homes cost twice as much as local incomes can support. But much of California has always been less affordable.

Nationally, to get back to the average affordability since 1980, meaning median houses are about 20 percent cheaper than the median family can afford, mortgage rates would have to come down to about 4.6 percent, while wages would need to rise 4{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb} and prices stay stable, the NAR’s Evangelou said. Wage growth has recently cooled a little, but remains above 4{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb} — in the recent nonfarm payrolls report, wages were up 4.4{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb} from a year ago, though a bit below the December gain of 4.6{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb}.

Mortgage rates remain volatile, and the market hopes that began 2023 — that the Fed would be cutting its benchmark interest rates before year-end — have recently dimmed as the labor market and consumer remain too strong to provide confidence that the current rates hikes are doing enough to slow inflation. After falling for five weeks, the average contract interest rate for 30-year fixed-rate mortgages increased to 6.39{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb} from 6.18{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb} last week, and was as high as 6.8{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb} on Friday. The rate was 4.05{171d91e9a1d50446856093950b947460c67b1ae5766d3d173ffede4594e3fbfb} one year ago.

How fast could affordability get better? On a $300,000 loan, a drop in fixed rates to 4.5 percent from today’s 6.75 percent, with no change in prices, would change the monthly payment by about $425 on a 30-year loan, about a 23 percent drop. Going to 6 percent cuts a payment by about $150, or 8 percent. A 5 percent income gain this year for the median buyer would add about another $400 a month.

“If rates come down to 5 percent, it gets radically better very fast,” Olsen said.

In a place like Tampa where prices grew rapidly during Covid, the affordability fix will probably blend near-stagnant prices for a year or two, pay raises and lower interest rates, Clarke said. But hotter markets like Tampa may need more price cuts to get affordability all the way back to historical averages, Evangelou said.

The market’s standstill is likely to last for months, at least, because its main underpinnings aren’t going anywhere. Sellers will continue to have the advantage of being equity-rich and sitting on a low interest rate from 2021 or before, Mohtashami says. Some buyers will remain priced out of the market, or able to afford less house than they want. And some will use work-arounds like mortgage buydowns or parental support to buy houses until affordability recovers. Sellers of new homes will do buydowns and have been using incentives since last summer to limit cuts to list prices.

“It has become kind of the norm,” Neuder said.

In some markets, affordability is likely to remain a problem for long enough that policy solutions will be needed, Olsen said. She mentioned solutions like building more dense housing, or letting more homeowners add additional dwelling units such as basement or attic apartments to let families share costs.

In most places, the likely outcome is affordability that falls somewhere between today’s market, where many prospective buyers are stretched and demand is light, and the buyer’s delight that prevailed for close to a decade. The path to that is rising wages, declining inflation that lets interest rates fall, and home prices that give back a still-to-be-determined chunk of the 2021-22 gains – a share that so far is small in most places.

“I want it to be flat the next two years,” said Clarke, the Florida broker. “You can’t rise 20 percent a year for a decade. You end up with a $5 million dollar two-bedroom, two-bath.”